Canada is world-renowned for its mortgage debt but it’s not as vulnerable to rising interest rates as other countries. Well, some other countries. Credit-giant Fitch Ratings ran mortgage stress testing on various economies. Canada’s variable rate mortgage borrowers are vulnerable to some shock, though nothing that can’t be handled. It may surprise many, but due to the relatively small share of variable rate mortgages, the country won’t see as big of an impact as countries like Australia and the UK.

Debt-To-Income Shock

The debt-to-income ratio (DTI) is the monthly cost of servicing mortgage debt compared to disposable income. Disposable income is the amount of income that remains after mandatory deductions. Bond and fixed income data is used to help establish their base assumptions. They’re looking at originations since 2020 and how they’d respond to a 3 point increase in cost by the end of 2023.

The end result is a view of how global mortgage markets will be impacted by the shift in funding costs. Bigger shifts generally indicate higher risk, however small ones aren’t unrisky per se. A smaller shift would contribute less to instability, since it’s a small change to the respective country’s economy.

One last point worth mentioning is Fitch Ratings assumes that income will be flat over this period. Stagnating wages aren’t typical of a high inflation environment with such a tight labor market. This means they are likely biased to more risk than reality, which is always a good thing when stress testing.

Canada’s Variable Rate Borrowers To Be Hit, But Not As Bad As Some Countries

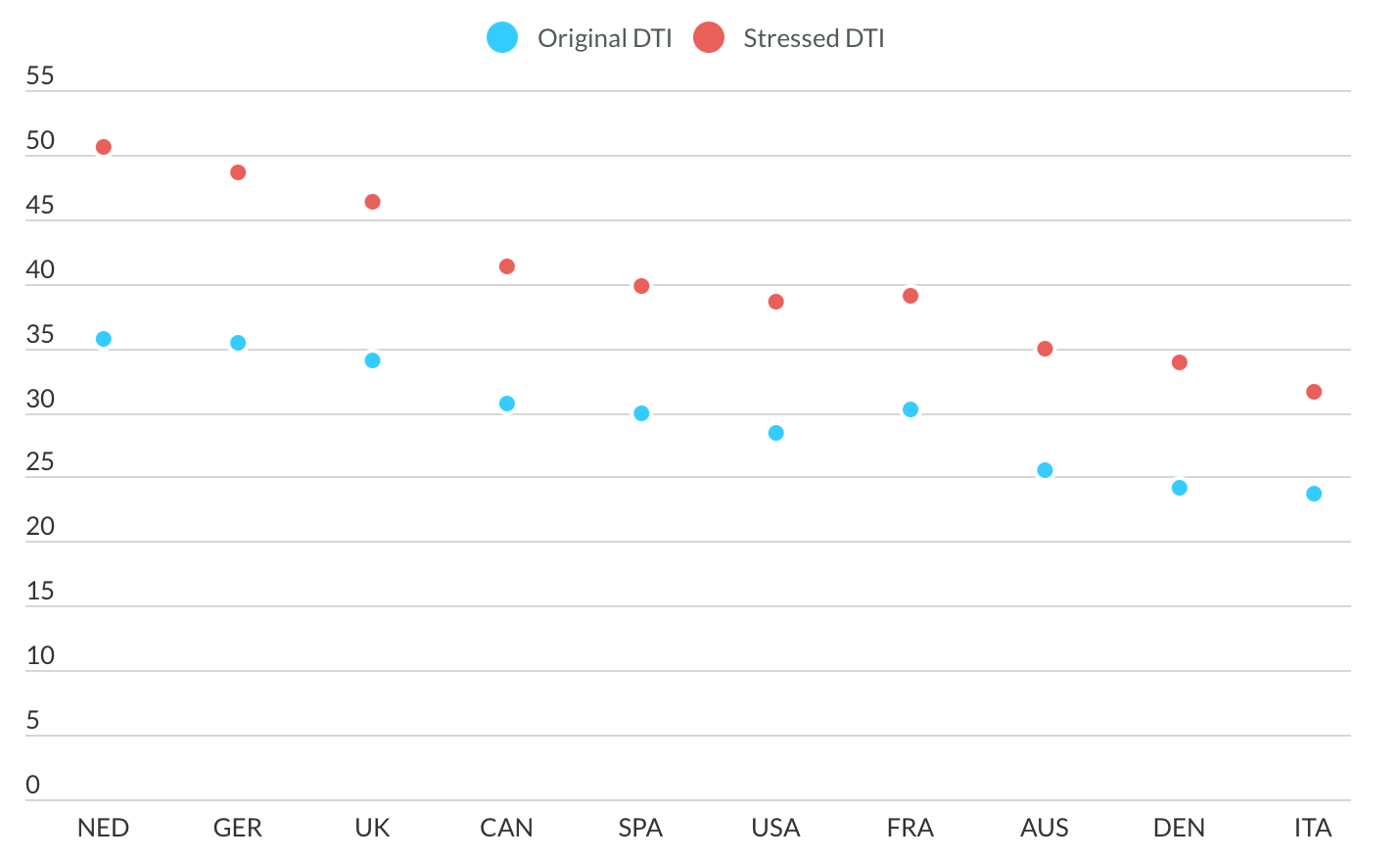

The credit ratings giant sees variable rate mortgage borrowers seeing a substantial surge in variable costs. Canada’s variable borrowers have an average DTI of 30.74%, meaning that’s the average share of disposable income used to service the debt. By the end of 2023, it’s forecast to hit 41.3% more than 10 points higher. That’s a massive jump, though Canadians tend to qualify with their gross income. Unless their tax rate is less than 10 points (very unlikely), this is still within their qualifying rate before hitting the stress-tested maximum for households.

Debt-To-Income Ratio Sensitivity For Variable-Rate Mortgages

The debt-to-income ratio for variable-rate mortgages in various countries from 2020, and the forecast impact of rates rising 3 points at the end of 2023.

Source: Fitch Ratings.

Despite Canadian households being highly indebted, they aren’t as sensitive to variable-rate shocks as other countries. The analysis shows the Netherlands, Germany, and the UK are more sensitive in this situation, seeing as much as a 15 point increase.

Countries like the US are more inline with Canada’s bump, though still more affordable.

Canada Isn’t As Vulnerable To Variable Rate Shock As Australia

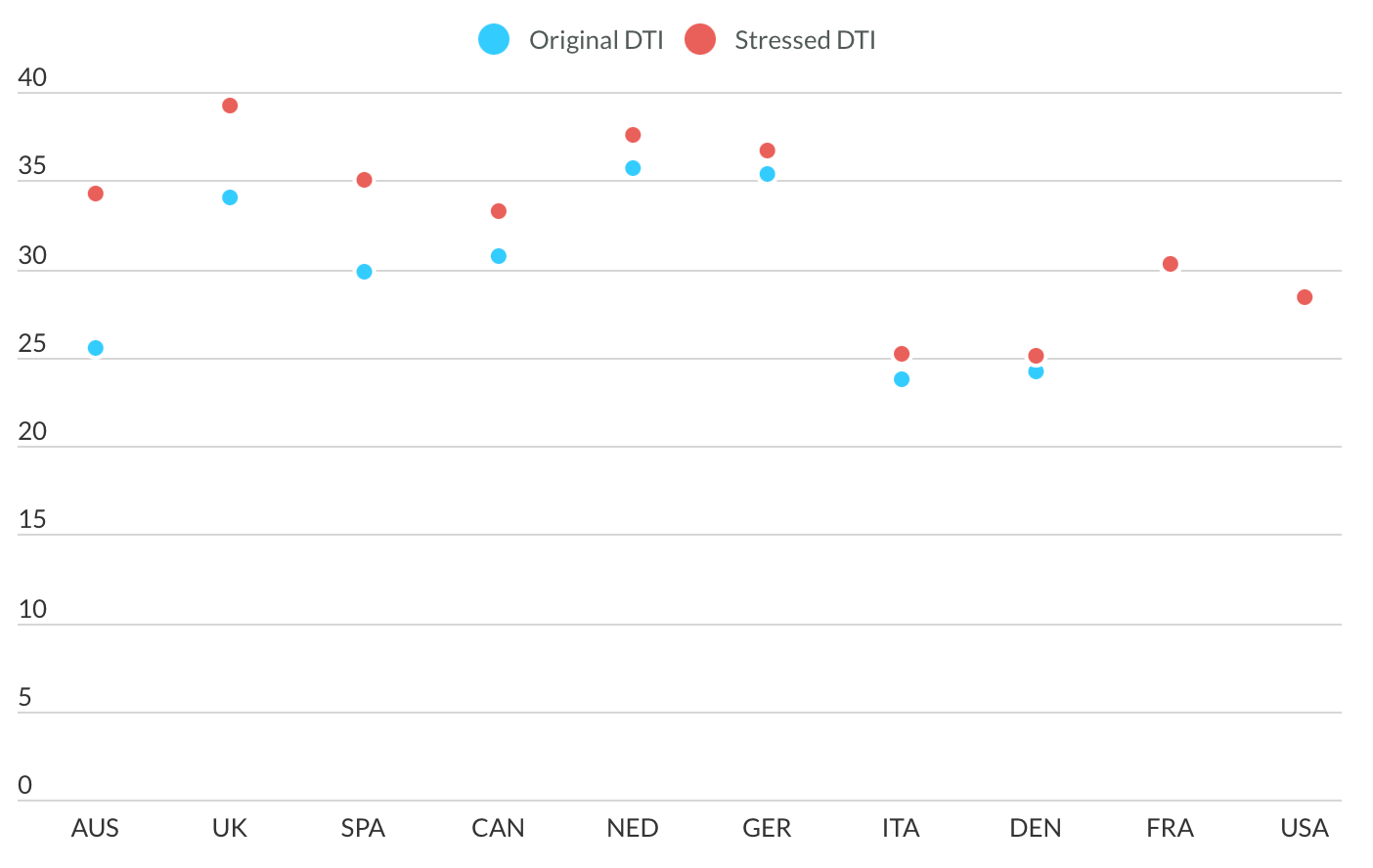

The total mortgage market, including fixed-rate mortgage debt, reveals a totally different picture for Canada. Canada’s DTI goes from 30.74% to 33.29%, since the majority of debt is fixed rate. It wasn’t until last year that Canadian mortgage borrowers suddenly wanted variable rate debt. Households opting for fixed rates traditionally helps to prevent rising rates from introducing sudden risk.

Debt-To-Income Ratio Sensitivity For Variable and Fixed-Rate Mortgages

The debt-to-income ratio for variable and fixed-rate mortgages in various countries from 2020, and the forecast impact of rates rising 3 points at the end of 2023.

Source: Fitch Ratings.

Interestingly, that’s not the case with some of the world’s other biggest residential real estate bubbles. Australia, Spain, and the UK will experience the biggest shocks due to a heavier reliance on variable rate mortgages these days. Worth emphasizing that the spike of around 9 points in Australia only places it slightly higher than Canada.

There’s a lot of takeaways, but disposable income and the shift in cost are the two biggest to keep in mind. The higher this rate is, the more households will have to divert funds from consumption to debt servicing. Higher debt loads mean more future economic growth was borrowed to support housing costs. This tends to slow down the economy long term.

The shift in cost is what Fitch Ratings is focused on, in this analysis. The slower things move, the more time they have to adjust. When things change quickly, an economy has much less time to adjust to the shock of diverted funds. This can lead to a sharper, stronger hit to the local economy.

In the case of Canada, starting with a high debt load presents a growth and opportunity risk over the long-term. However, the Fitch Ratings analysis shows rising variable rates won’t be as big of a shock as it will be in economies like Australia and the UK.

Canada “Better than Australia” in terms of the size and volatility of our housing bubble is like when we say our health care is “Better than the U.S.” Like, yeah, it better be, or else we’d be totally doomed. Damnation by faint praise.

Well said